Business

TransAct is a thermal printing company transitioning into a food service technology platform.

The company has three revenue streams:

- BOHA!

In this segment, the company offers a hybrid value proposition between hardware and software. They sell food service terminals, SaaS software and label consumables. This replaces pen-and-paper back-of-house food safety workflows.

Basically, the employee taps a touchscreen on the terminal, the terminal prints FDA-compliant date/allergen label instantly. The terminal is connected to the kitchen appliances. For instance, fridge temperatures are logged automatically via IoT sensors. If you have multiple chains like QSR or large department stores, through the terminal, corporate sees real-time compliance across all locations.

The hardware-software bundle here is the moat. Pure software competitors cannot print FDA-compliant labels, they need separate hardware. The recently launched BOHA! Terminal 2 has 3” wide thermal printers built in that enable dual-column nutrition panels required for grab-and-go food. This expands their TAM because large department stores usually offer grab-to-go sushi and sandwiches. The terminal runs proprietary BOHA!OS, no alternative software runs on it. Switching means replacing hardware simultaneously. Label consumables create recurring revenue that pure software companies have zero equivalent to.

- Casino & Gaming

The company sells TITO (ticket-in, ticket-out) thermal printers and EPICENTRAL software for casino floors.

TACT and JCM Global (Japan) are the two dominant TITO ticket printer suppliers globally. This is the system inside slot machines that prints barcoded vouchers instead of dispensing coins. Regulatory certification requirements in every jurisdiction make new entrants essentially impossible. Sales flow through OEMs like Light & Wonder rather than direct to casinos, creating some concentration risk but also deep stickiness since switching printer vendors requires re-certifying the entire slot cabinet in every jurisdiction.

On top of the TITO hardware sits EPICENTRAL, a real-time casino marketing platform delivering targeted promotions directly to slot machine screens and printed tickets. This is mostly optionality, not meaningful.

Casino and Gaming is not a growth engine and OEM exposure makes sales lumpy. Nonetheless, it generates free cash flow that funds the BOHA! Transition.

- Legacy- McDonalds Ithaca 9000 kiosk printer

Melting ice cube, not worth addressing.

Installed Base Opportunity

- Active Terminal 2 units: 19959

- Legacy AccuDate / T1: ~40000

- ARR annualized (Q1 2026 run rate): 13,2M

- ARR CAGR 2019-2025: 36%

Original BOHA/ Terminal 1 have a maximum label width of 2,2 inches. FDA-mandated dual-column nutrition panels for grab-and-go food require more than 2,2 inches. This is a physical constraint, no software update fixes it. Every operator entering the grab-and-go market must upgrade regardless of satisfaction with current labeling. These customers already believe in it. The conversation shifts from “replace your working terminal” to “your current terminal can’t do the new thing you want”.

There are two independent growth engines. The most sexy of those being new logo wins, like sushi franchises, QSR chains, convenience stores, corporate food service etc. But one underappreciated growth engine is T1 conversions: 40k relationships, existing label revenue, no concept-selling or pitching required.

Management’s ARR target on existing customer base is a 100-200USD uplift per machine per month in the long run ( whatever that means). At midpoint 150*19,959= 35,9M ARR, nearly 3x current run rate, without shipping a single new terminal.

OEM Channel: Apple and MedVantage

TACT distributes BOHA! through two hardware form factors. Terminal 2 is the all-in-one proprietary unit. The BOHA! Workstation pairs an iPad with a label printer peripheral and BOHA! software. Apple’s enterprise iPad sales team becomes an indirect channel into every restaurant kitchen. MedVantage distributes BOHA! to US healthcare food service under their GoFreshDate brand, hospital cafeterias where compliance burden exceeds QSR and switching costs are higher than their traditional customers.

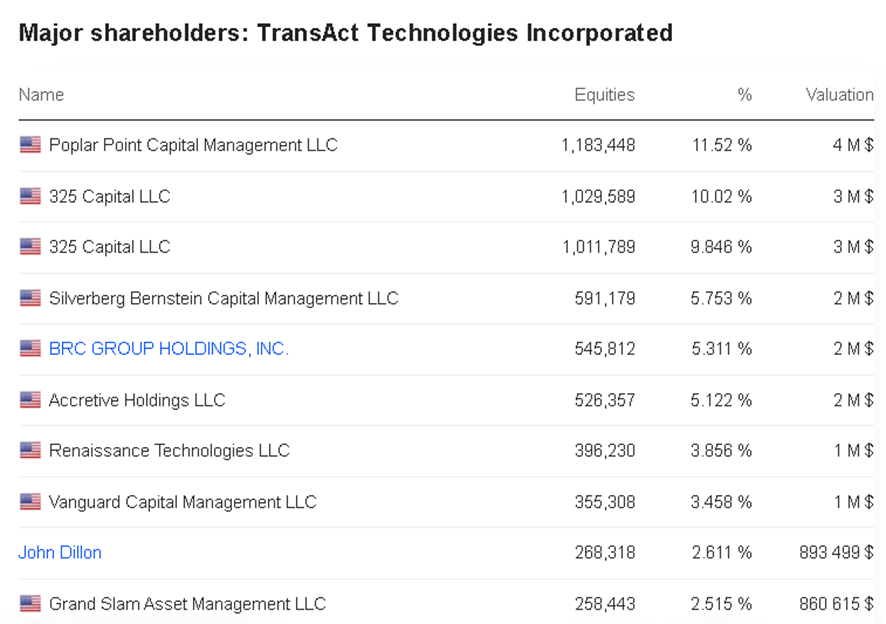

John Dillon and the Toxic Ex Syndrome

The new CEO, besides buying 350k on the open market @3,49-3,56, has an interesting track record.

He was a nuclear submarine officer for 5 years in the US Army, where he designed engineering systems for submarines. Then, he went and had tenures at Oracle (sales) and early days Salesforce. He was also CEO at Navis (B2B software for marine container terminal operations) and ultimately sold the company to Zebra Technologies. He has been a Board member at TACT since 2011 and was appointed CEO in 2023 when the ex-CEO, Schuldman, resigned. He is an advocate of the software proposition of TACT. The source code acquisition, the new 3,5M share buyback program and the app store vision make sense for someone who has built and sold software platforms before.

Nonetheless, the company has also had its fair share of drama. First, succumbing to the pressure of activist investors, decided to launch a strategic review in 2024. There were preliminary discussions on partial or full sale. In May 2025 this was suspended, citing macro uncertainty and Q1 2025 record terminal sales momentum. This is essentially just the activist investors giving green light for management to execute. The timing proved to be ideal, since momentum in FST sales, especially greenfield, has slowed substantially since.

Then, one year after suspending the strategic review, Schuldman (ex-CEO), issued a letter to management, essentially saying they don’t understand what they are doing. Schuldman spent 3 decades of his career at TACT building a hardware company. Dillon believes the company should pivot to software. Schuldman thinks software ambition is an overreach, because they can’t outspend SaaS native competitors (even if this is not the current management’s intention). Dillan thinks owning the software is what makes the label business permanently defensible. Both have merit and neither is selling shares, the current CEO is buying.

The company’s share ownership structure, with Poplar Point, 325 Capital and Accretive Holdings owning a meaningful portion of the company’s shares ensures continual supervision and zero tolerance for value destruction. The 325 nominated director is inside the boardroom with full visibility.

The numbers

The framing here is that you are paying 22M for the operating business of a company generating 14M in quarterly revenue, with a casino duopoly, 20k active BOHA! 2 Terminals and growing ARR.

The cash here also acts as a cushion of downside protection and if the business delivers I think it can double or triple in 3-5 years.

Risks

- Large QSR permanently use Terminal 2 as a dumb label printer, never convert to SaaS, ARPU depressed. 30-40M recurring becomes unachievable by any standard. Watch Q2-Q3 2026 for conversion language.

- Casino OEM revenue is super volatile, only have to check previous years

- Thailand tariff exposure: 100% manufacturing in Thailand post China migration. Baseline universal tariffs under current trade regime. Any escalation compresses margins.

Gonçalo