(This article is from October 2025. Stock went up a lot, time to revisit)

History

Bonterra Energy Corp. is a long-standing oil and gas production company. Historically, it was a focused Pembina Cardium play. The Pembina region of the Cardium has long been a petroleum-producing hub in Alberta in terms of pure conventional oil, i.e., low-hanging fruit. Unfortunately for society and investors alike, the times of conventional Cardium are over. With advances in technology, in particular horizontal drilling and multi-stage fracturing, oil recovery was enhanced and the Cardium is in fashion again. In the Cardium, drilling locations tend to have shallower depth, which contributes to lower well costs.

I couldn’t find any reliable sources from recent years, but I estimate from researching companies active in the area that sustaining breakeven costs are between $55–$60 WTI, meaning that at today’s oil prices some producers are already unprofitable (to the surprise of absolutely nobody).

Things changed for the company in 2024. On March 1, 2024, it closed an acquisition to purchase primarily undeveloped petroleum and natural gas assets in northern Alberta (Charlie Lake) for a cash consideration of $23.6 million CAD. The Charlie Lake asset is located northwest of Grande Prairie on a contiguous 118 sections of land. This is a game changer for the company, as you will see after.

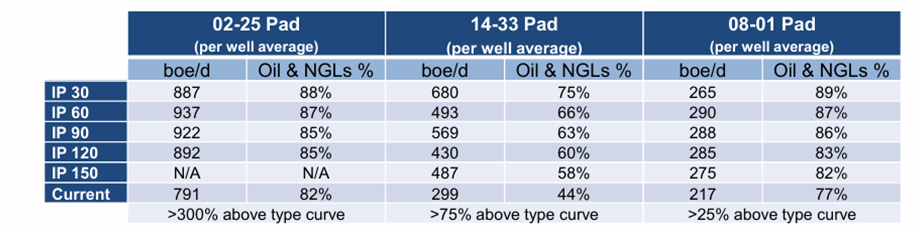

Then, the company also proceeded, in November 2024, to de-risk the Montney asset it already owned, with 52 sections of contiguous land, of which only 10 are booked. The first Montney well has been flowing unrestricted since November 2024, and the early results of its second well are impressive, with 915 BOE per day. The Montney asset is located directly north of Grande Prairie, Alberta (Valhalla). This asset provides massive optionality.

Cardium

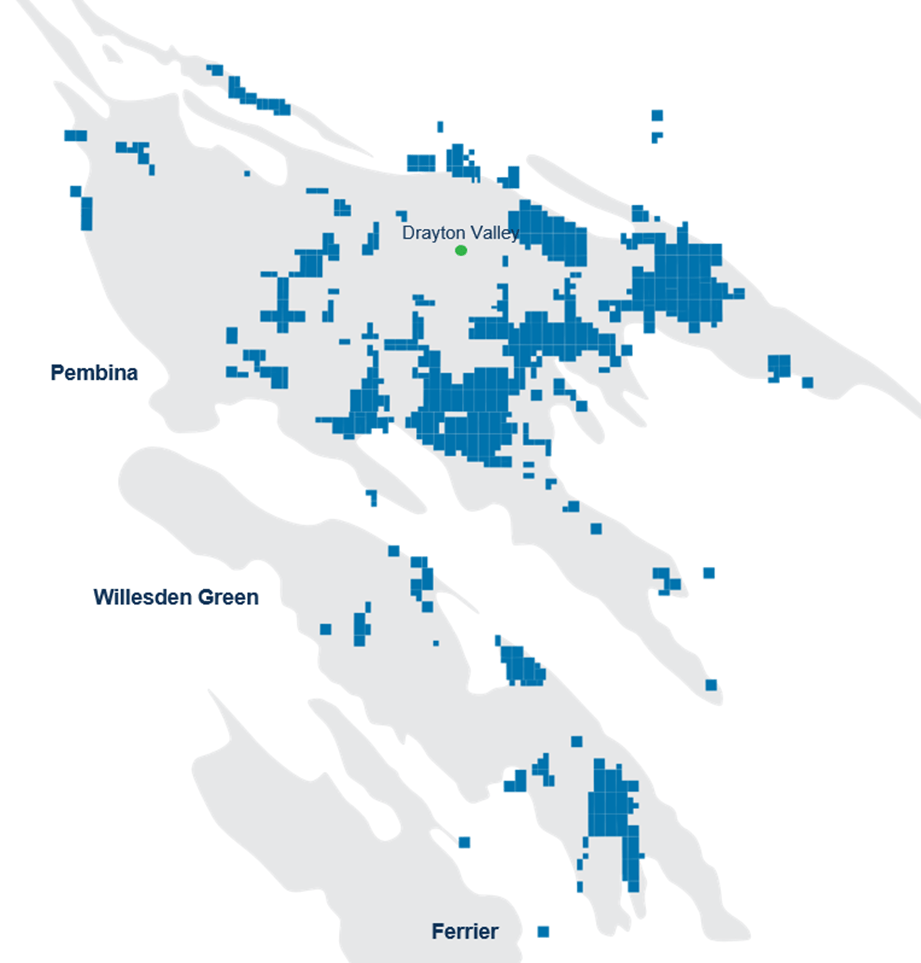

The Cardium is the principal asset of Bonterra Energy Corp. and, prior to 2023, it was effectively the company’s sole producing play. The Pembina Cardium, where most of Bonterra’s production is situated, represents the largest conventional oilfield in Canada. Although “conventional” only in legacy terms, as most current production now relies on modern drilling and completion methods, its foundation remains the same prolific reservoir. Bonterra also owns complementary Cardium assets in the Willesden Green area. Altogether, the company holds approximately 312 gross (284 net) sections in the Cardium, with around 284 booked drilling locations.

The Cardium is often described as the “lifeblood” of Bonterra. It provides stable production volumes and consistent field netbacks. In recent years, the company has evolved its development approach, adopting horizontal drilling, pad development, and multi-stage fracturing, all of which have improved recoveries and reduced costs. For example, the use of pad drilling from sites with existing infrastructure has enhanced operational efficiency, helping Bonterra maintain relatively stable production costs despite industry-wide inflationary pressures.

To understand why the Cardium remains such a differentiated play, it helps to look at the underlying resource base. The formation contains an estimated 10.6 billion barrels of original oil in place (OOIP), of which only about 15% has been produced to date. The adoption of horizontal drilling and modern completion technologies has meaningfully improved recovery factors while reducing the cost per incremental barrel.

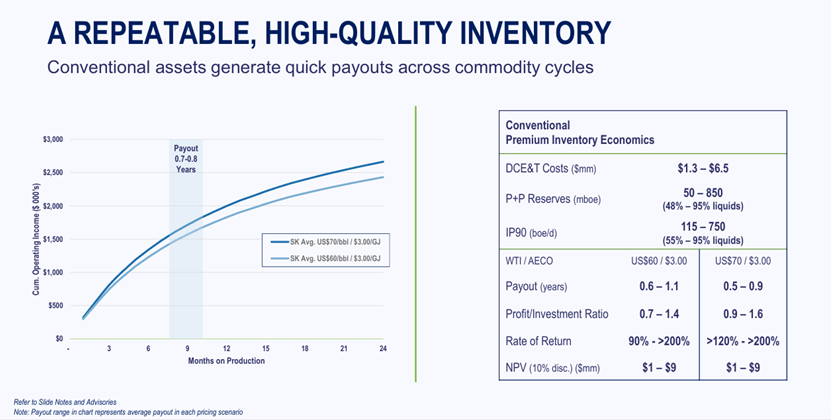

Compared with other Western Canadian plays such as the Montney or Charlie Lake, the Cardium is more oil-weighted—producing a higher proportion of crude oil relative to natural gas and NGLs. This allows Bonterra to retain strong exposure to oil prices and capture a larger share of benchmark WTI-linked pricing. Well economics in the Cardium are highly attractive, and development is relatively straightforward and repeatable. Drilling and tie-in costs are substantially lower than in deeper or more technically complex formations like the Montney, mainly because the Cardium is shallower and geologically simpler. Consequently, well payouts are excellent: in Bonterra’s case, IRRs can exceed 70%, with typical payout periods of around 1.25 years at mid-cycle prices. Some peers, such as InPlay Oil, report even stronger returns in certain parts of the play.

It’s worth noting, however, that these economics are price-sensitive—returns moderate meaningfully at lower oil prices.

Because the Cardium is a light-oil, conventional-style reservoir, decline rates are shallower than in shale or tight-oil operations. Bonterra’s corporate decline rate of roughly 21% includes both mature legacy wells and new horizontal wells. This represents a moderate decline profile for a light-oil producer—not overly steep, but sufficient to require steady drilling of replacement wells to sustain production levels.

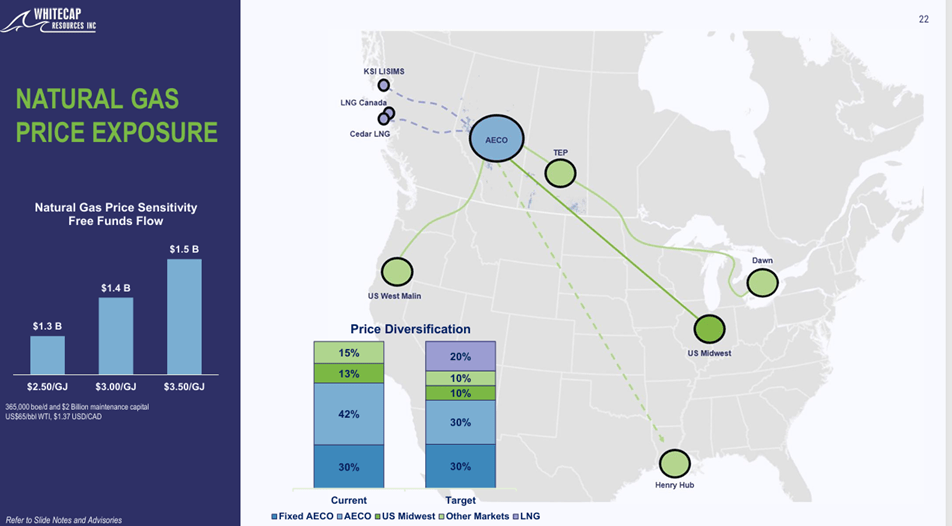

Another strategic advantage of the Cardium is its location and connectivity. The play is well positioned within central Alberta’s mature infrastructure corridor, which links to multiple midstream systems and refineries. While the Cardium is not a direct supplier to Canada’s upcoming LNG export projects (such as LNG Canada, Cedar LNG, or Ksi Lisims), it stands to benefit indirectly from the broader expansion of Western Canadian gas egress capacity and midstream investment. The region also enjoys relatively good access to U.S. markets and faces fewer egress constraints than heavier oil regions like the oil sands, supporting better realized AECO gas pricing.

Additionally, Cardium light oil and condensate are in strong demand from oil sands producers, who use them as diluent to blend with bitumen for pipeline transport. This provides a reliable local market and helps maintain regional price stability.

From a technical perspective, the Cardium’s value is well understood by the market. With only about 28 unbooked locations (assuming one well per location) remaining and the rest already captured in Bonterra’s 2P reserves, investors ascribe little incremental upside to this asset. The reasoning is simple: the company is too small to aggressively develop both the Cardium and its newer plays simultaneously. As a result, the market assigns limited credit to future reserve growth from the Cardium, at least for now.

Charlie Lake

Bonterra acquired the Charlie Lake asset in 2024, consisting of 79 net sections of land in the Bonanza area, for a cash consideration of CAD 24.1 million. Combined with the company’s previously held 37 net sections, this brings Bonterra’s total Charlie Lake position to 116 net sections, of which only ≈8.2 locations have been booked.

Unlike the Cardium, Charlie Lake still carries high optionality, as it is in the process of being de-risked. Currently, only about 7% of the resource is booked. Assuming that roughly 40% of internally identified locations can be converted to booked status over the coming years, and using an internal estimate of 220 Mboe per well, the total potential resource would be around 10,136 Mboe, equivalent to ≈1.73 years of current production at Bonterra’s rate.

In 2025, the company constructed a new battery to support operations, and the area benefits from ample gas egress options, similar to the Cardium. Well economics are stronger than in the Cardium, while decline rates remain comparable. IP365 averages roughly 387 BOE/d, with slightly higher liquids exposure than the Cardium. At normalized WTI prices, IRRs can exceed 100%, with correspondingly shorter payback periods.

Under current capital constraints, it is understandable why Bonterra prioritizes Charlie Lake. Each well contributes approximately CAD 3.5 million in NPV10, and with 10 wells expected by 2025, the total NPV could reach ≈CAD 35 million, exceeding the price paid for the asset. Production is projected to reach ~6,000 BOE/d within five years, achievable by drilling 5–10 wells per year in line with current CapEx expectations.

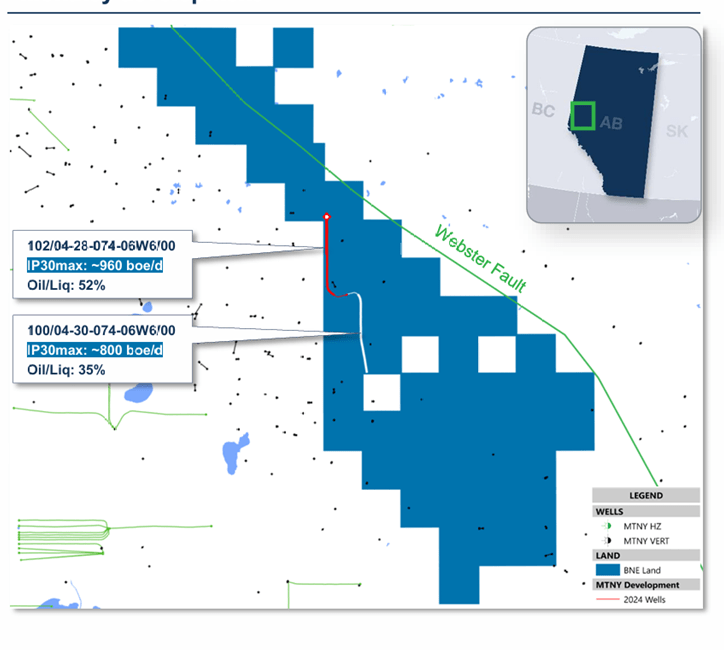

Montney

The Montney represents a world-class liquids-rich light oil and gas play for Bonterra, with a very long development runway. To date, the company has drilled two wells, both of which have produced positive results, demonstrating the asset’s potential.

Drilling and tie-in costs in the Montney are higher than in the Cardium or Charlie Lake, but well payouts are short—under one year, and the IP365 averages around 668 BOE/d. Each booked location contains roughly 880 Mboe of 2P reserves, with 10 locations currently booked. In addition, Bonterra has identified over 95 potential locations internally. Assuming that 20% of these locations are eventually booked, the Montney could add approximately 16,720 Mboe of incremental 2P reserves, equivalent to nearly three years of current production at Bonterra’s current rate.

Arbitrage between assets and NAV

Bonterra currently has 106,070 Mboe of 2P reserves. As Charlie Lake continues to de-risk, an additional 10,136 Mboe can reasonably be booked, and Montney could add 16,720 Mboe. Under these conservative assumptions, total reserves could grow to ≈132,926 Mboe in the coming years, effectively adding 2–3 years to the Reserve Life Index (RLI) — and this assumes no contribution from the Cardium. A rough NAV estimate under different oil price scenarios looks as follows:

| Case | Realized Price (C$/bbl) | Pre-Capex Netback (C$/boe) | After-Capex (C$/boe) | NPV10 (C$M) | Debt (C$M) | Shares Outstanding (M) | NAV/share (C$) | P/NAV | Fair Value (C$) |

| High | 65 | 34 | 27 | 2,514 | 165 | 36.59 | 64.20 | 0.25 | 16.05 |

| Mid | 46 | 20 | 13 | 1,209 | 165 | 36.59 | 28.53 | 0.25 | 7.13 |

| Low | 30 | 4 | –3 | ≈0 | 165 | 36.59 | 0 | 0.25 | 0 |

Even at mid-cycle prices (~CAD 46/bbl, or WTI ~$75), and using a P/2PNAV of 0.25x, the company appears over 100% undervalued. At the high-case scenario (~CAD 65/bbl, WTI ~$90–95), Bonterra could be worth multiples of its current market capitalization. This analysis underscores the critical importance of management execution.

Bonterra generates approximately CAD 30 million in free cash flow per year after CapEx, representing ≈24% of its current market capitalization. Management has also approved a NCIB to repurchase up to 10% of the float, providing additional shareholder value.

The company has mentioned potential accretive acquisitions, which could be value-accretive if they materially de-risk the Charlie Lake and Montney assets. Otherwise, it is difficult to identify similar-quality assets at a better valuation than the current stock price.

Gonçalo