Business

PeopleIN is one of the largest Australian workforce solutions companies, operating as a family of specialized recruitment and labor-hire agencies. The company screens, recruits, trains, and employs casual, part-time, and permanent staff for over 4,200 clients. Since its IPO in 2021, PeopleIN has remained responsible for all wages and remuneration, charging customers based on hours of work performed.

It operates across several high-demand, compliance-heavy sectors—notably Engineering, Trades and Labour, Food & Agriculture, and Professional Services (IT, Accounting). These sectors are characterized by persistent labor shortages; PeopleIN provides essential value by handling screening and paperwork, allowing customers to focus on core operations.

Acquisitions & Dispositions

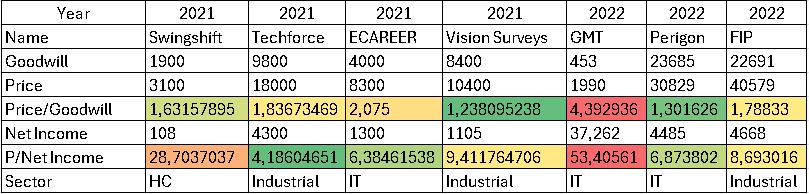

Due to the fragmented nature of the industry, PeopleIN has engaged in substantial M&A. To assess the price paid for individual businesses, I have focused on the multiple of goodwill, as these are relationship-heavy businesses where value resides primarily in goodwill.

Notable acquisitions are Perigon and FIP, in the IT and Industrial segment.

Perigon is an agency focused on finance, accounting and tech candidates for permanent and contract opportunities.

FIP is a leader in the agriculture and food segment, which is lower margin, but also more recurrent.

Capital Recycling

Recently, the company underwent a major capital recycling program in order to divest lower-potential segments into better opportunities. They started by divesting Techforce; they acquired Techforce for 18M and sold it for 23,5M. During these four years, Techforce has earned 17M in profit, which suggests a 126% return in 4 years (IRR 22,6%). Then, they divested the Health and Community Business for 20M, or 6.2 times FY25 earnings. This was above the multiple the company traded at, so all-in all good capital allocation. More recently, after completing the divestments of Techforce and H&C, they announced the acquisition of Infrawork. Infrawork is New Zealand’s largest provider of skilled migrant contract labour and migration services. I think this is a good match, because they can leverage the pipeline of candidates from Infrawork to place their candidates in infrastructure business ahead of the construction boom leading to the Brisbane Olympics in 2032. The acquisition was done at a maximum payable (including earn-outs) of 3.7x EBITDA.

Where we stand now

Because this is a balance sheet first story, we will start by seeing the financial position and the health of the company in that department. Net debt in H1 2026 stands at 13M, or 0.6x pro-forma EBITDA. Following the acquisition of Infrawork and the completion of 6m share buyback, this should come up to 1.5x. This is the lowest in history and gives the company some flexibility in terms of acquisitions and capital allocation. Regarding profitability, we are still early in the recovery process. Engineering, Trades and Labour has seen a surge in normalized EBITDA, but this is mostly related to cost cutting initiatives rather than a fundamental recovery in the business. Food & Agri remains steady, despite a sharp decline in billed hours due to lower candidates under the PALM scheme. Professional services remain depressed, but no major collapse in EBITDA. The company is taking a proactive approach to increase investment in leadership roles to drive additional sales.

Where we go from here

The company generates 50%+ of its revenue from Queensland. Queensland is entering a major infrastructure cycle with demand for over 50k additional workers expected through FY29 and is positioned as one of the primary workforce engine for this growth. They can also use use the PALM scheme to fill domestic labor gaps (especially in agriculture). Bill rates have not collapsed, which means that the company’s pricing power has not eroded. Having around 5% market share in Queensland, in the base case they can grow their Engineering, Trades and Labour division 10% per annum until 2029. This would mean that, assuming no margin expansion, this division would grow to 22M EBITDA in 2029. Assuming no recovery in Food & Agriculture and Professional Services, we would be talking about 30M group EBITDA in 2029. At a 80% cash conversion, which is lower than what they usually achieve through the cycle, this would mean FCF of 26M, for a company currently trading at 73M, with aligned management (CEO owns 3M worth of shares for 400-500k base salary) and at what could be a near through in the sector. Some modest insider buying has been ongoing as well.

Risk/Reward

The risks are manageable, given the low leverage, prudent capital allocation and the market having been beated down for a while now. Nonetheless, I could see profitability eroding still. If EBITDA declines further 20% (PALM scheme delays, not being able to capture share from Queensland boom), then the company’s FCF could decline to 14M. At a beaten down fcf multiple of 4x, this means further 22% downside from here. The base case is for the company too make roughly 26M in FCF. If this happens, then the market could rerate it to 8-10x FCF, in line with a cyclical staffing company performing well. At 8x, this would imply 200M valuation, 170% upside from here. In conclusion, 3 year IRRs range from -8% in a bad but plausible scenario and 39% in a base scenario. A lot of volatility in expected returns.

What I will be watching

Moving forward, I will be watching leading indicators such as job advertisings and job vacancies. Over the next quarter’s for the company, I will be watching capital allocation, billing rates as well as revenue growth/stabilization and ebitda margins.

Gonçalo