Business

Euronet operates across three main segments:

- Electronic Funds Transfer (EFT): Euronet owns and operates its own ATMs as well as bank-outsourced machines, with a network of roughly 56,000 ATMs. This segment contributes about 30% of the company’s total revenue.

- epay: This segment distributes both physical and digital third-party content—think Netflix or Amazon gift cards. It makes up roughly 28% of revenue.

- Money Transfer: Through brands like Ria and XE, Euronet facilitates global remittances. There’s also Dandelion, a high-margin solution that lets other fintechs or banks leverage Euronet’s payment rails. While it’s a smaller portion of revenue, Money Transfer accounts for 42% of the total.

EFT

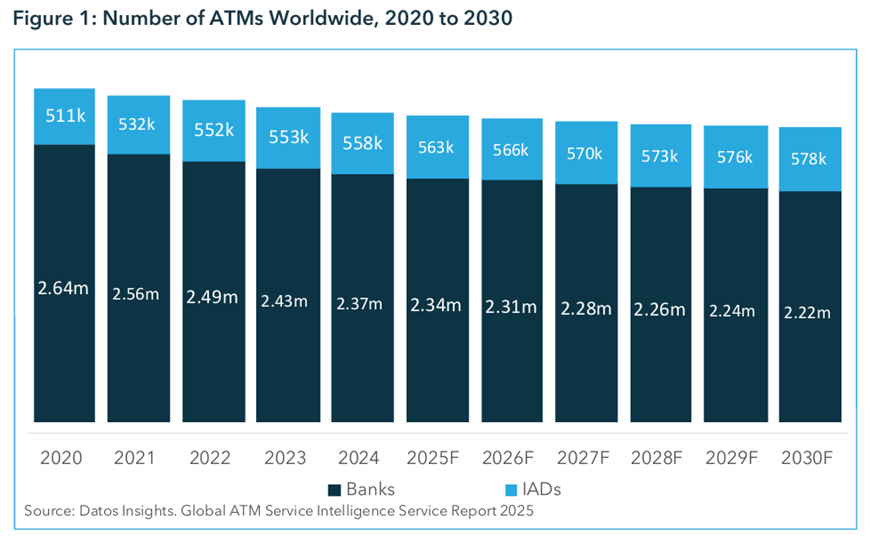

Euronet is one of the world’s largest independent ATM operators. It earns revenue from customer surcharges and dynamic currency conversion fees, as well as fees charged to financial institutions whenever their customers use independent ATMs. The challenge is that regulatory committees in various countries often prevent fee increases, so surcharges have remained largely flat. These committees, typically consortia of financial institutions, aim to keep interchange fees low. Combined with falling transaction volumes, this creates a double squeeze on margins.

Banks often operate ATMs at a loss, treating them as part of standard customer service. However, fee pressures and the rise of online banking are pushing banks to shut down ATMs—and even branches. This leaves room for independent operators like Euronet to continue consolidating the market.

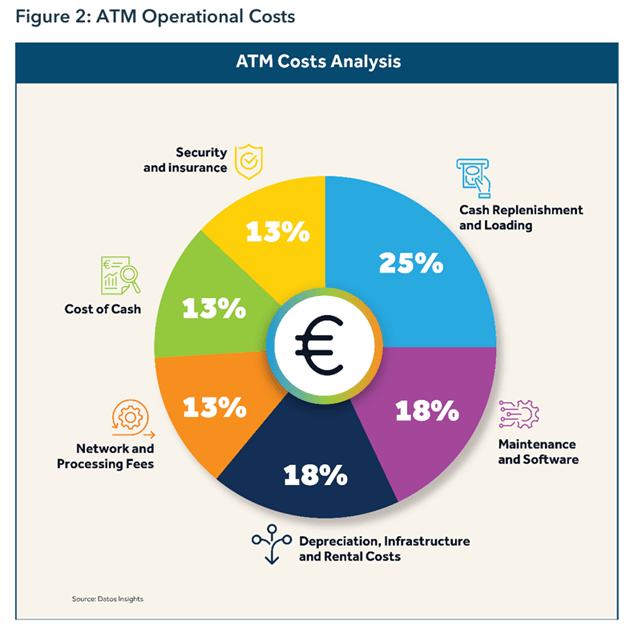

ATM operating costs are largely fixed. Because fees haven’t increased, margins have taken a hit. If regulatory bodies allow higher fees, Euronet could benefit from strong operating leverage, boosting profitability.

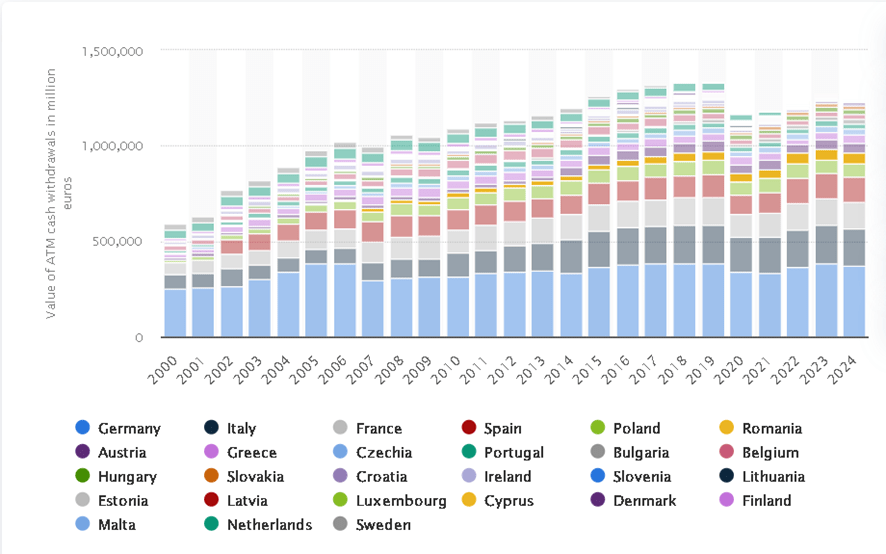

Having laid out the economic challenges, it’s worth addressing the narrative that ATMs—and cash—are dying. In my view, that’s simply not true.For me, this is simply not the case.

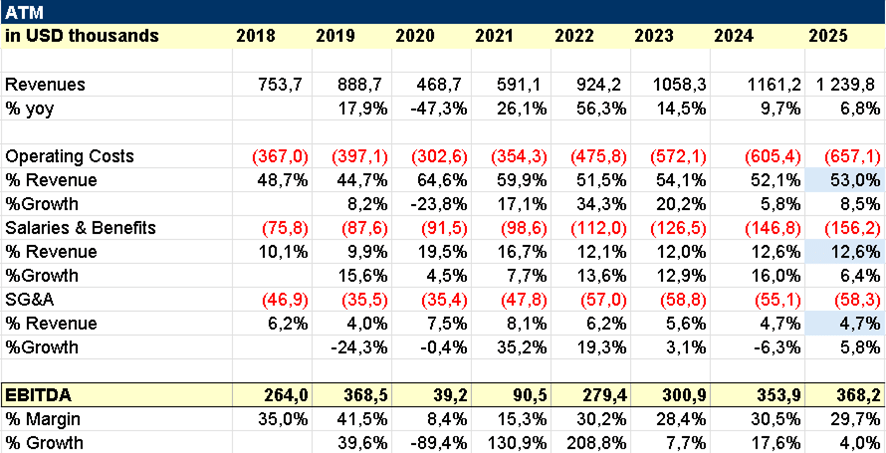

The ATM business has actually grown steadily, with revenues increasing at a 7.4% CAGR since 2018. EBITDA margins have been more volatile, reflecting the economic pressures discussed earlier. Looking ahead, Euronet’s strategy remains the same: acquire well-placed ATMs from banks and operate them. Since banks still control the largest ATM networks globally, there’s significant room for consolidation and growth. Margins are likely to stay flat or decline slightly, depending on whether regulatory committees allow fee increases, which hasn’t happened in years

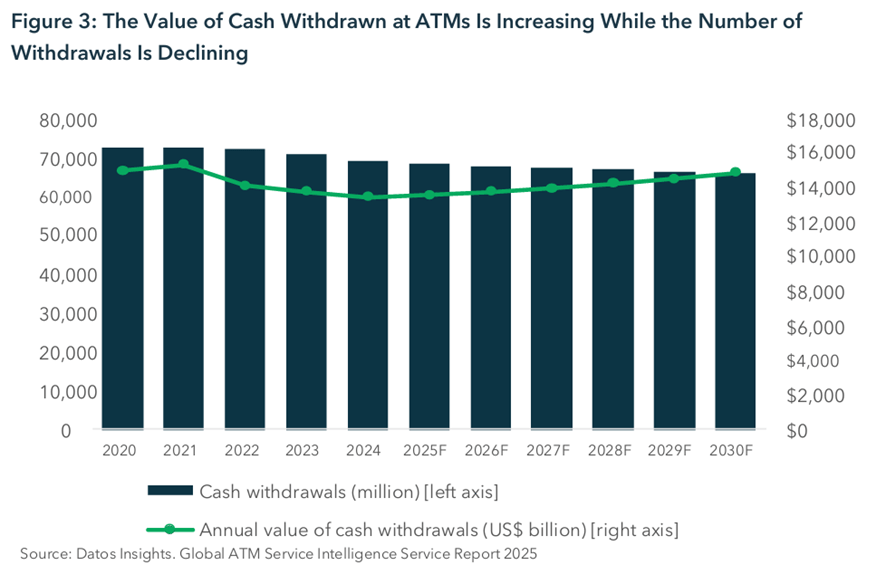

On the cash narrative: cash is far from dead. Around 90% of global transactions are still settled in cash. While ATM transaction counts are gradually declining, the value of those transactions is actually rising.

Even in highly cashless regions—like in Scandinavia—governments are actively encouraging people to keep cash, highlighting its importance in events such as power outages or other emergencies. So, what multiple does the ATM business deserve? Recently, NCR Atlas, a larger ATM operator than Euronet, merged with Brinks at 7.2x EBITDA. NCR is a stronger company, so for valuation purposes, a 6x EBITDA multiple for Euronet feels reasonable.

Based on projected 2025 numbers, assuming they hold, 6x EBITDA implies an EV of €2.2B. This suggests the market is only valuing the rest of Euronet’s business at roughly €1.4B.

Epay

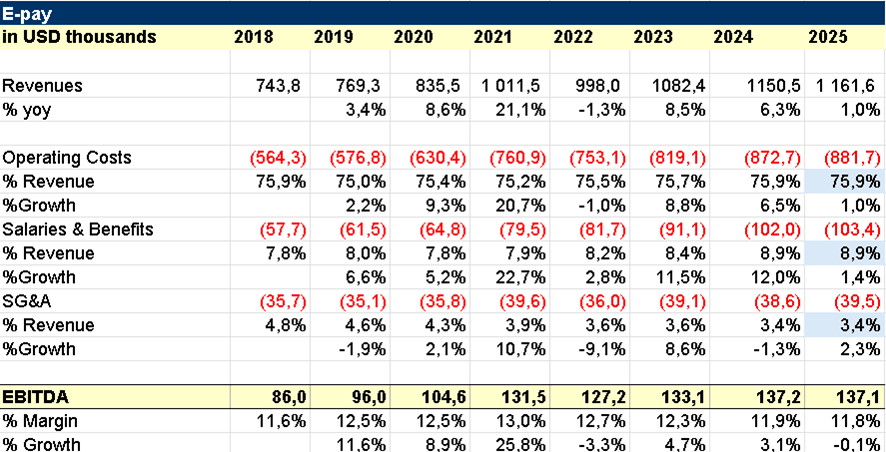

Epay is a distribution and processing network connecting brands like Amazon, Apple, telcos, and gaming companies with consumers through retail, digital, and POS channels. People use it to buy gift cards for birthdays, pay online more privately, or top up accounts. I admit I was skeptical at first—thinking, “who still buys prepaids in 2026?”—but it turns out there’s a steady demand. Its main customers are unbanked or underbanked populations worldwide.

Revenues have grown at a 6.5% CAGR since 2018, with margins surprisingly stable for a somewhat discretionary business. A relevant comparable is Paysafe, which trades at 6x EBITDA. Epay is better diversified: Paysafe relies heavily on gaming and gambling, which carries regulatory risk, while Epay works with a broad mix of household brands, telcos, and some enterprise clients. That gives Epay a more resilient revenue base, and in my view, it deserves a slightly higher multiple.

Paysafe has slightly higher EBITDA margins but grows top-line a bit slower (~6% CAGR) and doesn’t have the same strategic relationships with companies like Netflix, Amazon, or telcos for top-up services. Using a 7x EBITDA multiple for Epay, the segment contributes around €959M EV. When combined with the ATM business, the total EV comes to €3.16B versus Euronet’s current €3.23B market cap, which effectively means the Money Transfer segment is “free” in the current valuation.

Money Transfer

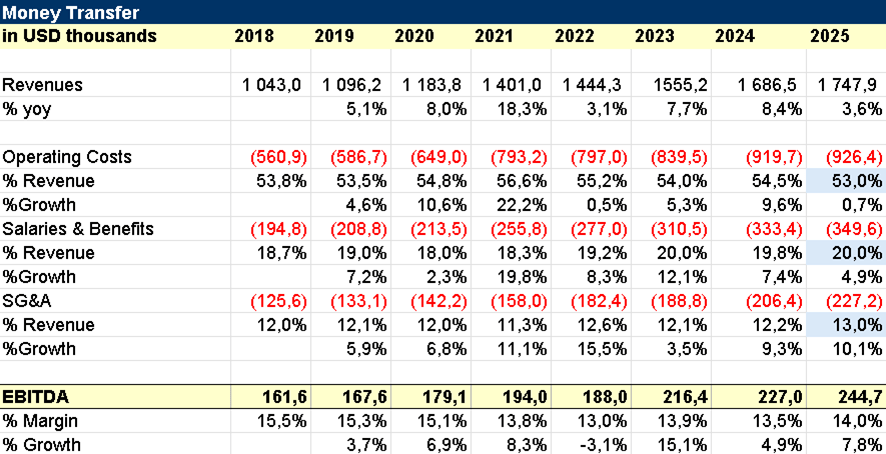

This is Euronet’s growth engine. Through brands like Ria and XE, the company facilitates global money transfers and remittances. There’s also Dandelion, which has evolved from a prototype into a high-profile solution for fintechs and banks, letting them leverage Euronet’s payment rails. While Dandelion is a small part of revenue, it carries very high margins—around 80%.

Historically, growth has been modest, around 7.6% CAGR, with slight margin compression. This is expected in a competitive environment, where digital-native players like Wise are lowering take rates to gain market share.

| Remittance Industry Comparison Table | ||||

| Metric | Euronet (Money Transfer) | Western Union (WU) | Remitly | Wise |

| Active Customer Reach | 95M – 100M+ (Est. based on physical/digital scale) | 100M+ active customers globally | 8.9M quarterly active users | 13M active people and businesses |

| Physical Payout Points | 600,000+ locations in 198 countries | ~600,000 (inc. 10k new Intermex sites) | 490,000+ cash pickup locations | 0 (Digital-only payout rails) |

| Quarterly Send Volume | Not Disclosed ($15T cross-border TAM focus) | Not Disclosed (Revenue: $1.03B) | $19.5B (Q3 2025) | ~$53.5B (£42.5B per quarter) |

| Take Rate (Rev/Volume) | ~2.60% (Implied by “20x 13bps avg”) | < 3.00% (Competitive pricing target) | 2.15% (Q3 2025) | 0.52% (52 basis points) |

| Digital Mix (% of Vol/Tx) | 54% of total volume settled digitally | 55% of all transactions are digital | Digital-First origin; high digital receive | 100% digital origin and payout |

| Reported Profit Margin | 35% (Incremental EBITDA margin) | 20% (Adjusted Operating Margin) | 15% (Adjusted EBITDA margin) | 13% – 16% (Target PBT margin) |

As you can see, in terms of customer reach, WU and Euronet are on a league of their own in terms of reach. They are the incumbents of the industry and have the advantage, especially in terms of having a large physical network and, in the case of Euronet, a big cash footprint.

Then, you have the digital winners, who are much more asset-light than the incumbents. Wise is fully digital-native and focuses on highly digital corridors. Unlike WU or Euronet, Wise doesn’t own its own rails—it relies on netting or plugs into partner banks’ rails. This allows Wise to focus entirely on customer interface and acquisition without investing in infrastructure, giving them very low cost per transaction. Wise has deep penetration in the corridors it focuses on, but it lacks the breadth and global reach of Euronet or WU.

Remitly sits somewhere in the middle. It’s not fully digital-native and still maintains some cash pickup availability. It specializes in certain corridors, particularly US-Mexico and US-India. Ironically, despite its modern approach, I think it’s the least well-positioned company overall, as it lacks scale and global breadth.

Euronet’s own money transfer business is targeting long-term revenue growth in the lower double digits, mainly from consistent market share gains in digital. Historically, it hasn’t grown this quickly, so I wouldn’t assume that as a base case. As of 2025, the company originates transfers in 60–65% of the global market, with plans to expand to 80–85% over the coming years.

What’s particularly interesting is that incremental margins are now very high (~35%), because the infrastructure is largely paid for and digital transfers carry higher profitability. Unlike pure-play digital competitors, Euronet’s digital channel is profitable by leveraging its physical payout network, not just digital innovation. Already, more than 50% of total money transfer volume is settled digitally, but it’s anchored on a decades-built global cash footprint.

This is why Euronet’s money transfer business is so “moaty.” Building a global cash network requires decades and massive liquidity, which makes it extremely difficult for digital-only players to compete in certain hard-to-reach corridors.

Valuing this segment is tricky. I wouldn’t pay 12x+ EV/EBITDA, but 5x feels too low. A reasonable middle ground is 8x, implying an EV of €1.9B. Combined with the ATM (6x) and Epay (7x) segments, the sum-of-the-parts EV is around €5.1B, versus the current market EV of €3.27B, signaling a ~36% discount to fair value.

The Big Picture

Instead of isolating each segment, I like to look at the company as a whole. Euronet is essentially an integrated payments platform—its ATMs, Epay network, and money transfer business all work together, with ATMs even helping facilitate money transfer exchanges.

Taking a conservative approach, I’d peg a fair value of around $109 per share, which implies roughly 66% upside from current levels. The upside isn’t explosive compared to some of the riskier names I follow, but the variance of returns is lower, and you still maintain the optional upside if the money transfer segment accelerates or surprises positively.

Risks

Euronet isn’t without risks. A large part of its business relies on immigrant populations sending money home, so shifts in immigration policy can directly impact transaction volumes.

Currency fluctuations are another factor. The company reports in USD but earns most of its revenue in foreign currencies, so changes in the Euro, British Pound, Indian Rupee, and others can materially affect reported net income.

Competition is intensifying. Digital-native players like Remitly, Wise, or Revolut have lower overheads and can offer more competitive pricing, putting pressure on Euronet’s margins, especially in digital corridors.

Looking further ahead, stablecoins and blockchain settlement rails could disrupt the traditional remittance model. These technologies may reduce the need for intermediaries and pre-funded liquidity, challenging Euronet’s core infrastructure.

Finally, regulatory pressure remains a constant. Dynamic currency conversion (DCC) limits and caps on interchange fees can constrain profitability, particularly in the ATM and EFT segments.

Gonçalo